Same Contribution Amount. Different Reward.

Dollar cost averaging is all about automatically investing equal dollar amounts at regular intervals (typically monthly). It’s a time-tested strategy and a smart alternative to trying to figure out market fluctuations and investing based on assumptions.

Setting up automatic contributions offers two significant benefits:

1. It takes emotion out of the equation and may help you avoid potentially costly financial

2. You automatically buy more shares when prices are low and fewer shares when prices are high, which can help you earn more over the long term.

Future Scholar’s automatic contribution plan offers an easy way for you to take advantage of this investment strategy.

Slow and steady for the win

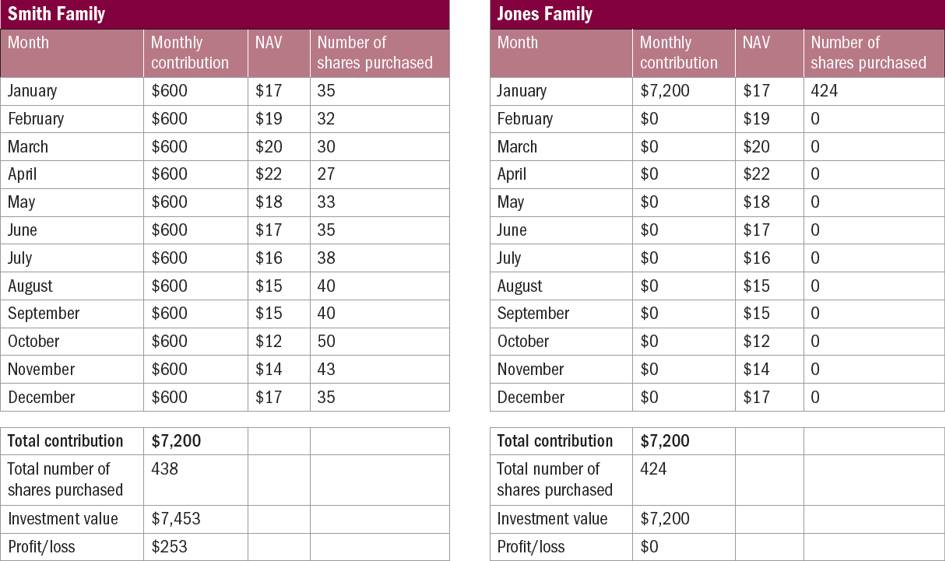

In the hypothetical examples below, the Smith family makes automatic contributions of $600 every month for a year, for a total of $7,200, while the Jones family makes a one-time contribution in the same amount in January.

Despite the total investment amount being the same, thanks to dollar cost averaging the Smith family ends up with a $253 profit by year end and owns 438 shares, while the Jones family has a $0 profit and owns only 424 shares.

Source: Columbia Management Investment Advisers, LLC. This example is for illustrative purposes only, assumes certain market conditions and is not representative of any particular investment. Market conditions change frequently; there can be no assurance that trends described would occur.